Laser Manufacture News:2018 China Laser Industry & Market Key Data

source:Laser Manufacture News

release:Nick

Time:2019-04-04

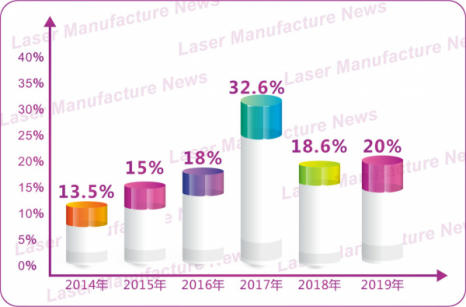

Introduction: In 2017, the market size of China's industrial laser and related products reached 72.1 billion yuan. In 2018, affected by the international situation and the ever-changing domestic environment, the growth rate of industrial production and sales in China slowed down, the investment in manufacturing industry was insufficient, and the downward pressure on the economy was large. According to the latest research data ofLaser Manufacture News, the market size of industrial lasers and related products reached 85.5 billion yuan in 2018, an increase of 18.6% year-on-year, and the growth slowed down. From the overall performance of the capital market in the whole year, China is growing to be global NO.1 market.

In 2018, the operation of private enterprises was very bad, but China’s economic operation was still fairly stable. According to the National Bureau of Statistics, in 2018, the average manufacturing PMI was 50.9%, and the overall manufacturing industry maintained growth throughout the year. Among them, food, wine and beverage refined tea, special equipment, railway, shipbuilding, aviation, aerospace equipment and other manufacturing industries are located above 57.0%, and the boom rate is rising.

In 2018, the demand for automated and intelligent production models in modern manufacturing is growing, and the demand for lasers is increasing. Meanwhile, the demand for laser equipment in emerging manufacturing industries such as semiconductors, panels, and new energy vehicles is growing. In 2018, high-power laser cutting and laser welding equipment continued to maintain the largest contribution to the Chinese laser processing market.

Geographical distribution map of China's laser market sales in 2018(note:亿= one hundred million)

According to the latest evaluation data ofLaser Manufacture News, the industrial laser output value of 85.5 billion yuan in 2018 is among the five major industrial belts of China's laser processing industry in the northwest, Central China, Bohai Rim and Northeast China, Yangtze River Delta and Pearl River Delta. They are 32 billion in South China, 19.4 billion in East China, 16.8 billion in Central China, 10.5 billion in North China, 4.3 billion in Northeast China, and 2.5 billion in other regions.

The reason why China's laser engineering application market trends have become the vane of the development of the global laser industry has benefited from the positive changes in China's economic restructuring in recent years, as well as the government's guidance and policy support for industrial development. According to statistics: the laser companies listed on the Shenzhen and Shanghai main boards, SME boards, and the GEM have a total performance of about 19.479 billion yuan in the first three quarters. These companies are outstanding representatives of the domestic laser industry. From their performance development, we can look at the domestic laser industry situation and development trend.

In 2018, the performance of most domestic laser companies will continue to show growth, but the growth rate will slow down. The author believes that there are four reasons for this: 1. China's economic environment is less than expected, and some local governments have returned to relying on infrastructure investment and real estate growth. 2. The impact of the Sino-US trade war. 3. The end user is on a wait-and-see state for laser equipment purchases due to the expected reduction in processing orders. 4. The demand for “laser + smart manufacturing” in the field of laser applications has not been released.

Annual growth rate of China's laser industry (Source: Laser Manufacture News)

Industrial lasers have always been the focus of the market competition, and fiber lasers still occupy an absolute market share in 2018. Demand for high-end equipment manufacturing such as laser engraving, laser marking, laser cutting, laser welding, laser medical and additive manufacturing is strong.

In 2018, global laser sales of nearly $15 billion (source:Laser Manufacture News), of which fiber lasers accounted for more than 58% of the global industrial laser market share. According to incomplete statistics: in 2018, the installed capacity of fiber lasers is more than 125,000 units, and the installed capacity of ultraviolet lasers has exceeded 10,000 units.

From the perspective of market structure, domestic brands account for more than 92% of the market share of low-power fiber lasers, and independent brand shipments dominate; domestic power accounts for about 55%; high-power is still dominated by foreign brands.

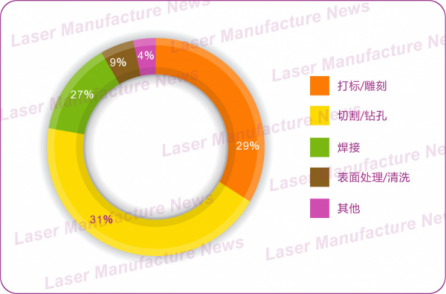

Market share of laser processing applications (orange: marking/engraving, yellow: cutting/drilling, green: welding, brown: surface treatment/cleaning, pink: other applications)

In 2018, shipments of sheet metal cutting equipment are still growing at more than 20%. It is estimated that the shipment of metal and non-metal laser cutting machines for macro processing will be approximately 22,000 units this year. The cutting market has more than 200 companies and the competition is still fierce. The demand for high-power cutting equipment for medium-thick sheet processing is exploding, and there is a trend toward high-power cutting. Ultra-high power laser cutting machines above 12,000W have attracted much attention, but the installed capacity in 2018 has not exceeded 100 units. The laser marking machine has shipped more than 130,000 units, the laser welding machine has shipped more than 8,000 units, and the laser cleaning equipment has shipped more than 700 units.

Demand in the 3C sector has declined compared to last year, mainly due to the slowdown in product upgrades in the consumer electronics sector and reduced demand for precision processing equipment. In 2017, the strong growth of the power battery industry entered the industry shuffling time, and domestic power battery companies shrank from nearly 400 in 2015 to 50 today. It will inevitably affect the demand for laser ear cutting and laser welding production lines for power batteries. Fortunately, the market for LCD panel, PCB, and wafer material processing is growing strongly. What is more noteworthy is that the plastic laser welding market is expected to move to the forefront, and demand will increase in volume in 2019.

The 2019 outlook. In the capital market: domestic and foreign capital will be added to the laser industry, the capital market may be devastating, and domestic laser companies should be fully prepared for this situation. Including United Winner, Maxphotonics, Wuhan DR Laser, Hymson, Bodor Laser, GD Laser, Grace Laser, YSL Photonics, JPT, Suzhou Delphi Laser, Wuhan Yifei Laser, Miracle Laser, etc. will accelerate the pace of entering the capital market. Who will be the next laser listed company after Raycus? Let us look forward to it. From the market perspective: the global entry into the 5G era, mobile phone materials and manufacturing processes will be changed to adapt to 5G new technology, a new round of business opportunities will bring huge economic benefits for laser equipment providers. In 2019, it gave 20% growth expectation in the field of electronic consumption. China's rail transit has entered the fast lane of rapid development. By 2022, the annual sales revenue of China's rail transit equipment industry will reach 872.5 billion yuan. The new energy vehicle manufacturing industry is undergoing technological upgrading, industrial transformation and manufacturing upgrades, and the integration of "laser + robot + automation control" technology solutions is its core. For laser companies, the rail vehicle and new energy vehicle manufacturing industry will be a huge blue ocean market.

In 2019, the market size of China's industrial laser and related products is expected to exceed 100 billion.

FISBA exhibits Customized Solutions for Minimally Invasive Medical Endoscopic Devices at COMPAMED in

FISBA exhibits Customized Solutions for Minimally Invasive Medical Endoscopic Devices at COMPAMED in New Active Alignment System for the Coupling of Photonic Structures to Fiber Arrays

New Active Alignment System for the Coupling of Photonic Structures to Fiber Arrays A new industrial compression module by Amplitude

A new industrial compression module by Amplitude Menhir Photonics Introduces the MENHIR-1550 The Industry's First Turnkey Femtosecond Laser of

Menhir Photonics Introduces the MENHIR-1550 The Industry's First Turnkey Femtosecond Laser of Shenzhen DNE Laser introduced new generation D-FAST cutting machine (12000 W)

Shenzhen DNE Laser introduced new generation D-FAST cutting machine (12000 W)